Grid investments in the Age of Electrification, AI and Data Ascendency

By Ron Pernick,

Clean Edge, Inc.

When Joel Makower and I cofounded Clean Edge back in 2000, we had a very clear sense that a host of emerging clean technologies – spanning renewables, the grid, transportation, and more – would experience learning curves and growth trajectories more akin to the internet and computers than to extractive energy sectors such as oil and gas. In hindsight, this thesis seems obvious, but at the time it was a radical concept that was just being embraced by a small cohort of tech and investment experts who had witnessed similar breakthroughs in the high-technology sector. After 25 years, clean tech and high tech are now firmly converging, especially at the intersection of the electric grid.

The statistics speak for themselves:

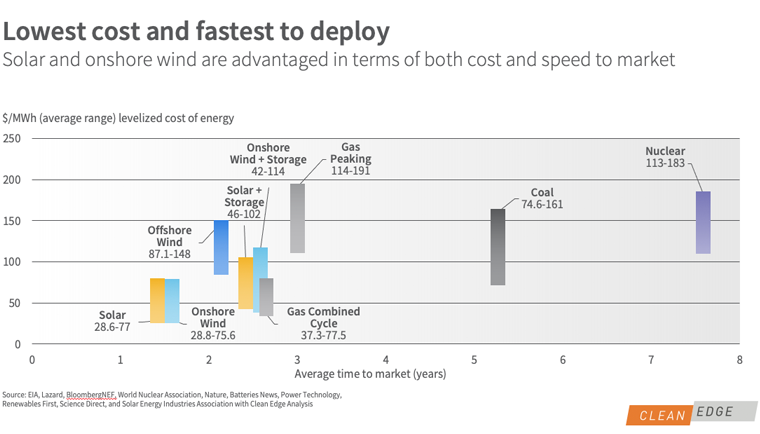

• Solar and wind are now the most cost-competitive and fastest-to-deploy sources of energy across most of the globe.

• Solar and storage have exhibited learning curves of 20% and 18%, respectively. A “learning curve” is the decline in cost for every doubling of manufacturing output globally – much like Moore’s Law for transistors on chips.

• Globally, on average, it takes nearly eight years to build a new nuclear power plant (much longer in places like the U.S. and U.K.) while it takes one and a half to three years to build a solar farm with integrated energy storage. New natural gas turbines are currently backlogged out to 2028-2030.

• In 2024, renewables represented a record ~90% of new electricity capacity additions both in the U.S. and globally.

• More than 17 million electric vehicles were sold worldwide last year and reached nearly half of all passenger vehicles sold in China, the largest global market by far with an estimated 11 million EVs sold.

• Datacenters are moving into the hyperscale, with Meta and others now building GW-size plants that require from 1 GW to 5 GW of operating power, enough capacity to power an entire city.

Which brings us to the electric grid. As renewables penetration grows, electrification of heat and transportation takes off, and new power-hungry AI-driven datacenters expand, the need for a modern 21st-century grid is not a “nice-to-have” but a necessity.

The electric grid is one of humanity’s greatest inventions. But amazingly, electric power pioneers Thomas Edison and Nikola Tesla, if somehow resurrected from the grave, would both generally understand the workings and mechanics of today’s grid. Imagine one of the original IBM mainframe engineers holding an iPhone 16 in their hand and you get the preposterousness of such a slow-moving, nearly static system.

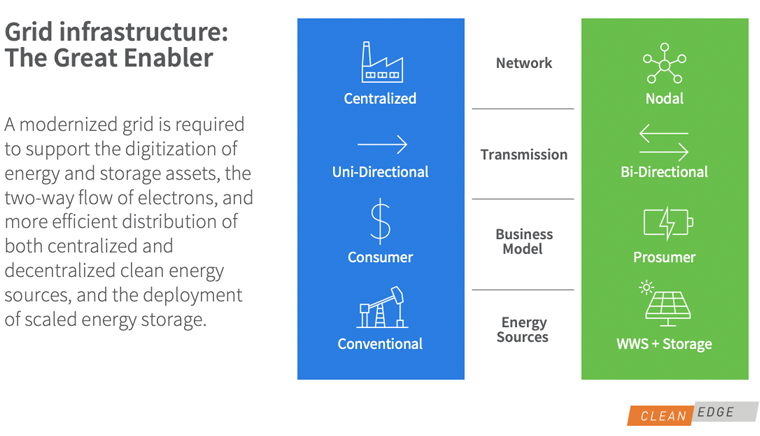

Yet after decades of inertia, we are finally witnessing a shift. As we highlight in the accompanying chart, we are moving from a centralized network to a nodal system; from one-way transmission flow to bidirectional flows; and from conventional centralized fossil fuels to a system increasingly dominated by solar, wind, and storage. At the same time, we are witnessing the advent of completely new business models, where users are not simply consumers, but are increasingly involved in providing energy and storage assets to utility grid operators – acting as “prosumers.”

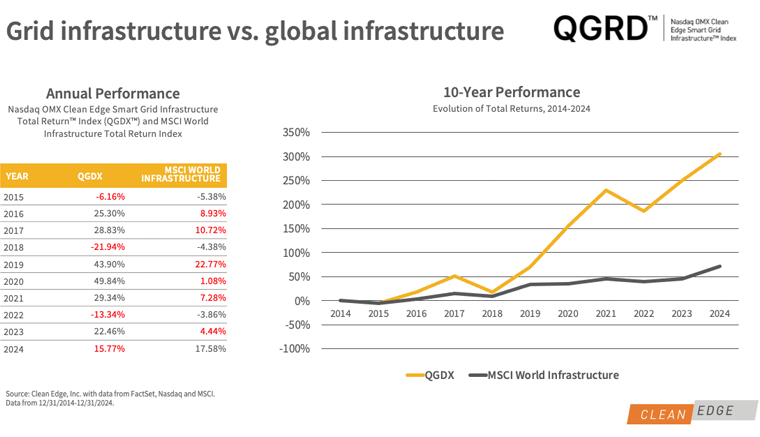

As the backbone of electrification, the global grid and smart grid infrastructure sector has become a growing focus for utilities, corporations, governments, and investors. Reflecting this trend, the Nasdaq OMX Clean Edge Smart Grid Infrastructure™ Index (QGDX™) has increased 305.14% over the last 10 years on a total return basis (see accompanying grid infrastructure vs. global infrastructure chart for more information). During the same period, the MSCI World Infrastructure Index, designed to capture the owners and operators of infrastructure assets globally, rose 71.51%. QGDX outperformed the MSCI World Infrastructure in six of the past 10 calendar years. After years of relatively flat power demand, the expansion of grid infrastructure is seeing unprecedented demand. BloombergNEF pegs grid expenditures at $24.3 trillion between now and 2050 and the IEA predicts 80 million kilometers (49.7 million miles) of new transmission and distribution (T&D) lines will be needed by 2040, approximately doubling the size of today’s global T&D networks.

Five key opportunities

Where do we see the greatest areas of opportunity in terms of both innovation and investment? While there are dozens of areas of innovation, below are five we want to highlight.

1) RE + Storage Baseload Grids

Renewable energy (RE) paired with large-scale storage is beginning to mimic the reliability of traditional baseload power, providing flexible, dispatchable capacity during peak demand. In states like California and Texas, massive deployments of lithium-ion batteries from players like Tesla and BYD have helped avert blackouts and stabilize grids during extreme weather events. Meanwhile, startups like Texas-based Base Power are pioneering ways for distributed assets to enhance grid reliability and resiliency at the grid edge.

2) Datacenters as an Asset

It might seem counterintuitive, but hyperscale datacenters — long considered energy-hungry liabilities — are increasingly being reimagined as grid assets. With on-site generation, load flexibility, and participation in demand response markets, they have the potential to support grid stability rather than strain it. Recognizing this dual role, regulators in states such as Oregon and Georgia are implementing policies to ensure that datacenters help finance grid upgrades, aiming to safeguard other ratepayers while maintaining reliability. Several companies and developers, as well as state regulators, are also looking at ways to reduce datacenter peak demand and emissions through demand-side-management and the deployment of storage and renewables.

3) Reconductoring Transmission

Rather than building new lines from scratch, reconductoring existing transmission corridors with advanced materials can significantly boost capacity and efficiency. Advanced conductors (often aluminum with a carbon composite core) can potentially double transmission capacity over existing corridors at less than half the cost of building new lines, according to researchers at the University of California, Berkeley and GridLab, a non-profit research firm.

4) Long Distance HVDC Lines

High-voltage direct current (HVDC) transmission is increasingly critical for moving power — from offshore wind farms, remote solar arrays, and hydropower facilities — to urban and industrial load centers across hundreds or even thousands of miles. While renewables are one key driver of HVDC growth, the technology is also being used for cross-border interconnections (particularly in Europe) and in stabilizing congested grids. Companies like Prysmian are laying undersea and continental HVDC cables that are redefining the spatial economics of electricity transmission.

5) Smart Meters 3.0

The next generation of smart meters goes beyond basic consumption data, integrating AI-driven analytics, real-time pricing, and bi-directionality. As next-generation meters and advanced metering infrastructure (AMI) evolves, it can enable a more resilient, decentralized grid where homes and businesses act as dynamic energy participants.

As developers of passive clean-tech indexes, our goal at Clean Edge is to create the most comprehensive and accurate benchmarks tracking clean energy, transportation, water, and the grid. In our partnership with Nasdaq, we have co-developed seven indexes which have $6 billion in AUM (assets under management) in exchange traded funds tracking our indexes globally (as of July 18, 2025, according to FactSet). They include CELS™ (U.S. listed clean energy), GWE™ (global wind), QGRD™ (global smart grid and grid infrastructure), HHO™ (U.S. listed water), and GHHO™ (global water).

While U.S. domestic federal policies and regulations can certainly impact index performance, there are a host of other factors impacting these market indexes, from global policy and regional economics to tech innovation and cost reduction trends. For example, if a decade ago I predicted that our clean energy index would increase 447% under a pro-fossil fuel Trump 1 and would decline 57% under the “climate presidency” of Biden, I don’t think you would have given me much credence. But markets aren’t just a reflection of the desires and policies of a presidency. In terms of electric grid performance, the benchmark QGRD acted very much like the infrastructure and utility sectors that it straddles – with the index up 128% and 55% during Trump 1 and Biden, respectively.

This is an unprecedented time in the history of electrification – an era filled with both anticipation and uncertainty. How will datacenters, hungry for massive amounts of electricity, build out new power sources rapidly and economically? Will Big Tech abandon clean-energy goals and shift to natural gas (if they can find the turbines)? Under what emerging models will long-distance transmission systems serve major population centers? Will energy storage see more traction in utility-scale or distributed models? How can electric vehicles and other distributed resources become grid assets?

Clean Edge will continue to monitor and benchmark these shifts as the electrification era accelerates — tracking not just market performance, but the transformation of the grid itself.

Article by Ron Pernick is cofounder and managing director of Clean Edge, Inc., where he oversees the development and production of the firm’s thematic research tracking clean energy, transportation, water, and the grid. The company is a joint developer of and contributor to the Nasdaq Clean Edge Green Energy™ Index (CELS™), launched in partnership with Nasdaq in 2006. Other indexes include the Nasdaq OMX Clean Edge Smart Grid Infrastructure™ Index (QGRD™), ISE Clean Edge Water™ Index (HHO™), and the ISE Clean Edge Global Wind Energy™ Index (GWE™). All tracking financial products of Nasdaq Clean Edge indexes exceeded $6 billion in assets under management as of July 18, 2025.

Under his leadership, Clean Edge has been at the forefront of researching technology, capital, and policy innovations driving the energy transition and grid and water infrastructure markets for more than two decades. He is the co-author of two books on clean-tech business and innovation, Clean Tech Nation (HarperCollins, 2012) and The Clean Tech Revolution (HarperCollins, 2007).

Disclaimer: Nasdaq® is a registered trademark of Nasdaq, Inc. and Clean Edge® is a registered trademark of Clean Edge, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor Clean Edge, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed or other publicly listed companies or Nasdaq Clean Edge proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.