Long before private equity firms raised their first fund or real estate investment trusts filed their first prospectus, land was wealth. Farmland is the oldest store of value in human history and the foundation of every economy that followed. Yet today, institutions own less than 2% of U.S. farmland.1 The entire institutional farmland market, roughly $50 billion, would barely register as a line item against the $33 trillion alternatives industry.2 Private equity, private credit, and commercial real estate dominate the conversation. Farmland, the original alternative asset, barely gets a seat at the table.

That is now starting to change, and the reasons go well beyond nostalgia for a simpler asset class.

The Numbers That Got Their Attention

In 2025, Nuveen launched a $3 billion private farmland REIT, the first of its kind from a major institutional manager.3 PGIM Real Estate now manages over $10 billion in agriculture.4 Pension funds, endowments, and sovereign wealth funds are building dedicated farmland allocations for the first time.

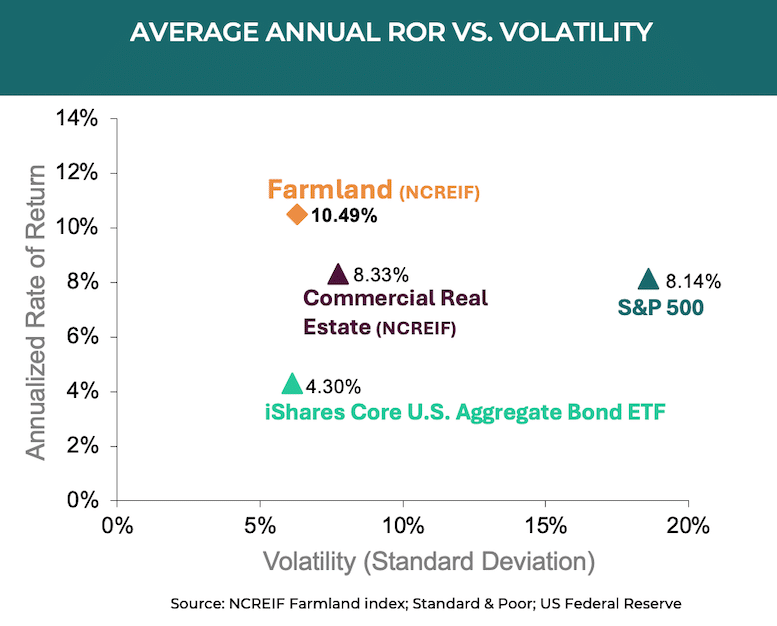

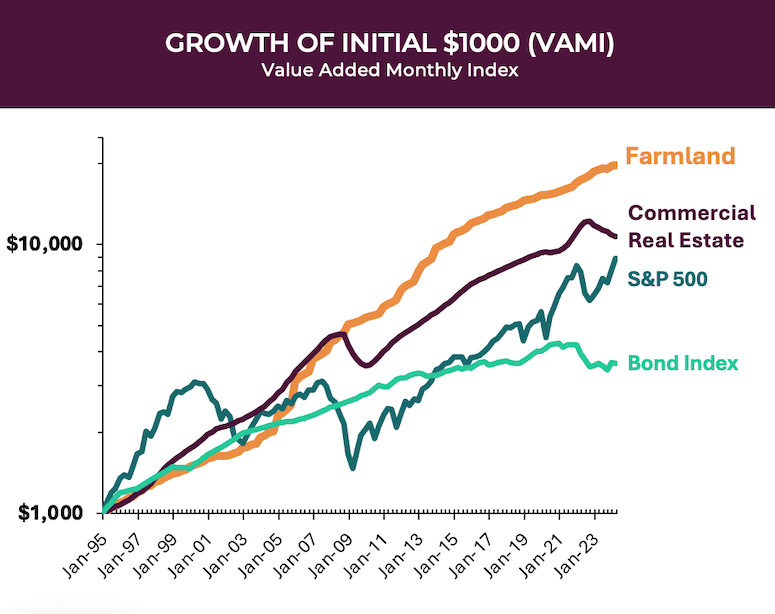

The performance data explains why. Since 1992, the NCREIF Farmland Index has returned 10.49% annualized, comparable to the S&P 500 which returned 10.65% and commercial real estate 8.33%.5 The difference is how it got there. Farmland delivered those returns with bond-like volatility: just 6-7% annual standard deviation versus 16-18% for public equities. The Sharpe ratio tells the story even more clearly with farmland at 1.2, and the S&P 500 at 0.3-0.4.6 That is three times the risk-adjusted return.

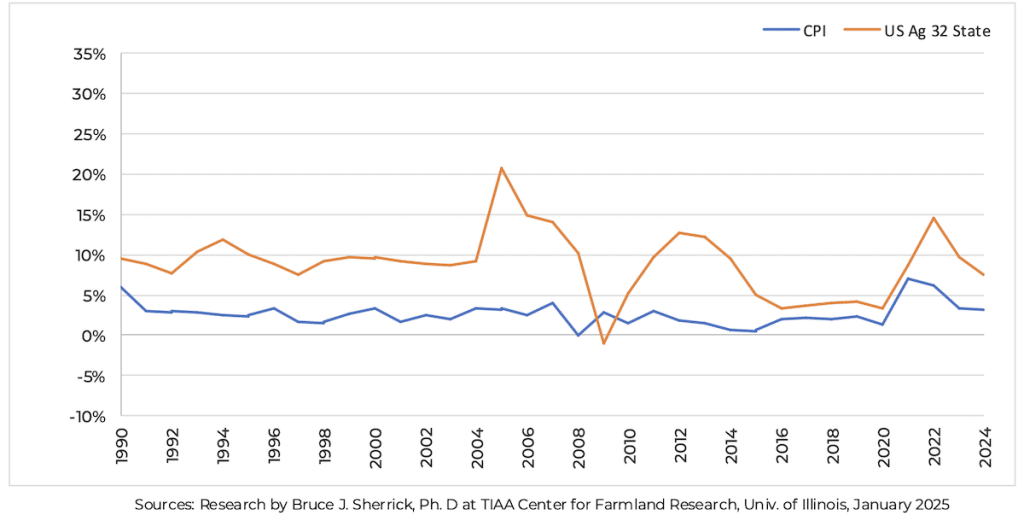

Farmland outperforms Inflation by 6%

Farmland also behaves differently from nearly everything else in a portfolio. Its correlation to equities is -0.06 and correlation to bonds -0.24.7 During the 2008 financial crisis, when the S&P 500 lost 46%, the NCREIF Farmland Index gained 17%.8 Since 1970, farmland has beaten inflation by an average of 6.6% per year, with its correlation to CPI jumping to 0.97 during the 2020-2022 inflationary spike.9 For allocators seeking a genuine inflation hedge with downside protection, farmland has a longer and stronger track record than gold.

The alternatives allocation in investor portfolios keeps growing, but the conversation remains narrow. Private equity, private credit, traditional real estate, and increasingly infrastructure absorb most new capital. Each depends on leverage, credit cycles, or discretionary demand, which are dynamics farmland does not share.

Private equity delivers strong returns, but its dependence on leverage is structural. Returns are engineered through financial structuring and exit timing. Farmland returns are driven by crop production and land appreciation, so it does not depend on financial structuring or a liquidity event to deliver returns.

Private credit has attracted enormous institutional capital, but it is ultimately a bet on credit cycles, specifically corporate creditworthiness in a rising-rate environment. That bet has reversed course quickly over the past two quarters.

Commercial real estate carries both leverage and discretionary demand risk. Multi-family real estate averages 51% loan-to-value (LTV), while offices sit at 78%.10 Add secular headwinds like remote work, retail decline, and office obsolescence, and entire sectors have repriced.

By contrast, farmland has just 13% LTV and enjoys secular tailwinds. The global population will reach 9 billion by 2050, requiring nearly double the current agricultural output.11 The average American farmer is nearly 60 years old, so as this generation retires over the next two decades, 300 million acres of farm and ranch land is expected to change hands.12 Meanwhile, the U.S. loses 2,000 acres of farmland per day to development,13 meaning it’s the only real asset class that is physically shrinking.

The demand driver behind all of it is the most durable one in any portfolio: food. People eat regardless of credit cycles, rate decisions, or geopolitical disruption. Non-discretionary consumption does not default.

The Third Dimension

Most investors evaluate farmland on two dimensions: how many acres, and what do they yield today. They make an implicit assumption that growing conditions will stay the same. Climate is the third dimension, and it is the one most portfolios ignore. The USDA projects a 12-29% decline in aggregate agricultural yields by 2050 due to changing temperature and moisture patterns.14 Florida’s orange production collapsed from 250 million boxes per year to roughly 12 million in 2025 as warming disrupted the frost cycles that kept disease in check.15 The federal government paid $19 billion in crop insurance claims over five years for climate-related losses.16 The assumption that growing conditions stay static is no longer defensible.

Sustainable Management is the Investment Thesis

U.S. farmland came through the 2008 recession unharmed, returning 9.2% while nearly every other asset class declined.17 That performance, combined with farmland’s negative correlation to equities and bond-like volatility, is what first drew institutional attention. What those early allocators discovered next strengthened the case: regenerative farmland management decreases risk and can deliver stronger financial returns than conventional farming.

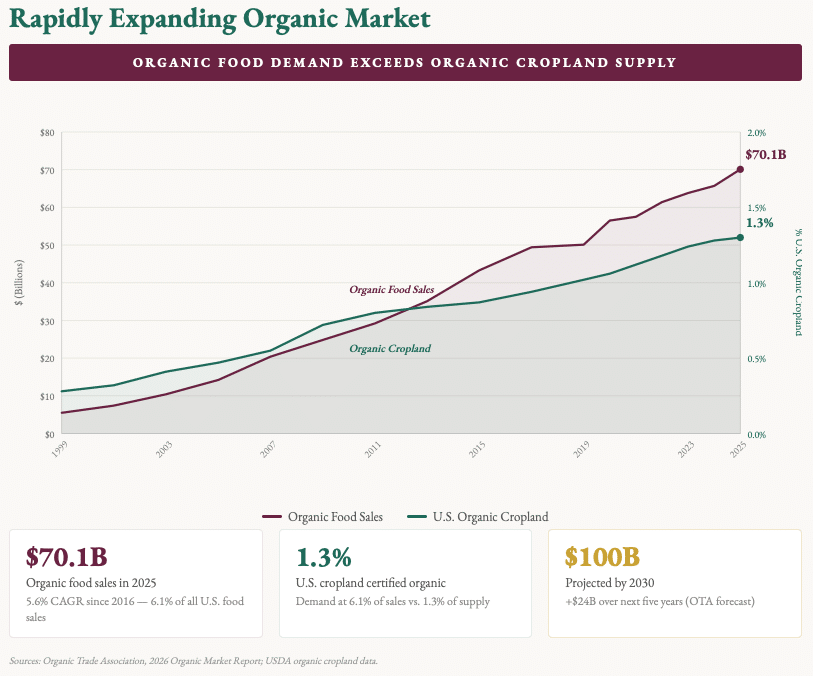

The organic food market hit $70.1 billion in 2025, representing 6.1% of all U.S. food sales, and the Organic Trade Association projects it will reach $100 billion by 2030.18 Yet only 1.3% of U.S. cropland is certified organic.19 That gap between 6.1% of consumer demand and 1.3% of supply is not closing. It is widening. For producers who can convert, it translates directly to pricing power with organic produce commanding 50-100% price premiums, and organic revenue per acre averaging 61% higher than conventional.20

But the advantage goes beyond pricing. Organic and regenerative systems lower input costs by eliminating dependence on synthetic fertilizers tied to volatile natural gas markets. They build soil carbon, which acts as a sponge, holding more water during droughts and absorbing more during heavy rain, reducing crop loss in both directions. These are not theoretical benefits. They are measurable reductions in operating risk that compound over time.

Two newer forces are accelerating this thesis. Regenerative farming practices can generate verified carbon credits through registries like Verra, creating an entirely new revenue stream per acre that did not exist a decade ago. And precision agriculture powered by AI is driving down costs while improving quality and consistency across large-scale operations. BCG estimated in 2025 that regenerative agriculture represents a $310 billion global investment opportunity.21 The USDA launched a $700 million Regenerative Pilot Program in December 2025 to accelerate adoption.22

Real-World Texture

At Farmland LP, we manage 19,200 acres of organic and regenerative farmland across California, Oregon, and Washington. We are not passive landlords. We are active farm managers, farming a portion of our crops directly through our farm operations team and leasing to experienced growers for additional crop programs. Across the portfolio, we grow over 40 crops and varieties, including blueberries, apples, wine grapes, almonds, hazelnuts, and cherries. We maintain core partnerships with Driscoll’s for blueberries and Stemilt for apples and cherries, and our fruit is sold at Costco, Whole Foods, Trader Joe’s, and your local grocery store.

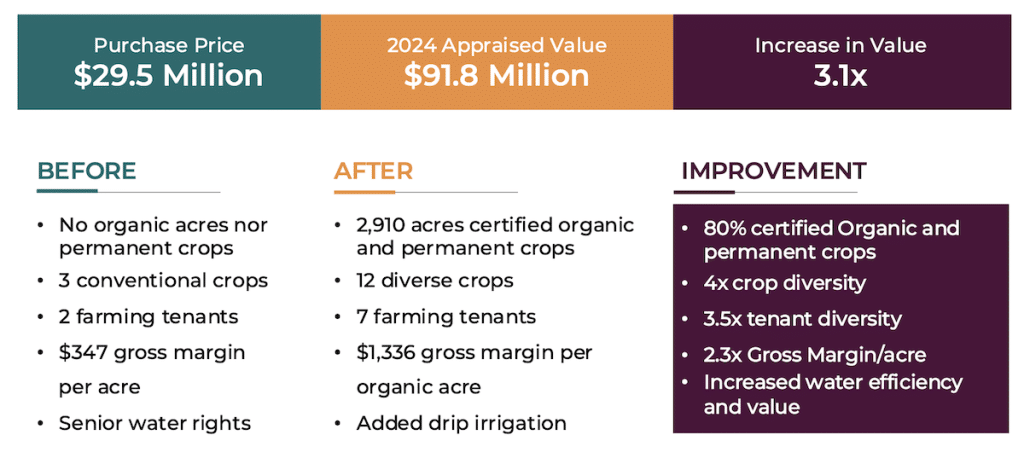

One property illustrates the model. We purchased Burns Farm in California in 2013 as a conventional operation, growing three crops with two tenants and a gross margin of $347 per acre. After organic conversion, crop diversification, and infrastructure investment, it now grows 12 crops with seven tenants with a gross margin of $1,336 per acre. A two-year USDA-funded study of our farming practices measured the impact of our efforts. The results were that in addition to a $32.5 million net investor gain, we generated a $21.5 million gain in net ecosystem value.23 Financial returns and environmental outcomes compounded together. Our organic practices improved our financial returns, and our scale increased the size of our impact.

The Window

Farmland is not a new investment idea. It is the original one. For centuries, farmland was the primary store of wealth. Then financial markets grew more complex, and farmland faded from institutional view even as it quietly outperformed.

The window for entry is narrowing. Supply is shrinking. Quality management is limited. Climate is reshaping where and how food can be grown. The investors paying attention now are not just diversifying their portfolios; they are making an allocation today to sustainably managed, productive farmland that is growing scarcer, more valuable, and harder to access.

Article by Craig Wichner, the Founder and Managing Partner of Farmland LP, a $350 million farmland investment firm managing 19,200 acres of organic and regenerative farmland across California, Oregon, and Washington. Named Agri Investor Farmland Fund Manager of the Year: Americas (2024), Farmland LP has been a certified B Corporation since 2010.