![]()

Lessons from the Pandemic

The world’s leading climate scientists have warned that we have only a few years left to keep global warming below 1.5°C, beyond which even half a degree more will significantly worsen the risks of drought, floods, extreme heat and poverty for hundreds of millions of people. To help guide policy making and discussion around the world, the IPCC has issued regular reports since 1988 drawing upon carefully constructed scenarios to predict the likely path of greenhouse-gas emissions and the resulting rise in global temperatures. The proposed scenarios must take into account not only complex scientific and environmental factors but also projections of population, economic growth, technology, and government policies.

For its Fifth Assessment Report, released in 2014, the panel collected a broad and numerous collections of possible scenarios, dubbed “representative concentration pathways” (RCPs) and selected four for deeper analysis. The most serious, RCP 8.5, is often called “business-as-usual” because it assumes no changes in government policies. To meet the recommended 1.5°C target will require emissions not just to stabilize but to decrease significantly. This would require drastic and immediate transformation of our human infrastructure, including how we generate energy and fuel our economy (IEA 2020).

Whether COVID-19 changes our collective mindset and lowers future emissions trajectories depends on whether it changes the path of the economy and investments in fossil-fuel usage or policy, moving beyond the business-as-usual scenario and introducing new measures such as carbon taxation. To date, reductions (Liu et al 2020) in emissions over the pandemic have yet to produce a perceptible change in concentrations, which are what affect climate as this years’ emissions come on top of century’s accumulated emissions. Though the economic consequences of locking down to quell the spread of the coronavirus will potentially eliminate many companies, it may also thwart the fast expansion of new infrastructure or renewable energy development aimed at reducing resource dependency. One interesting question to address now is how the overall growth trajectory of renewables will be impacted by this pandemic?

According to managers responding to Pensions & Investments\’ annual survey, U.S. institutional energy assets totaled $1.8 billion as of Dec. 31, 2019 down 35.2% from a year earlier and 43% from Dec. 31, 2014. Energy investments have been hit by a double whammy this year that includes falling oil prices with domestic crude prices falling to below zero in April, making renewables less competitive, and a worsening economic outlook due to the global pandemic. At the same time, energy managers are expected to invest more in renewables. Most investors expect that the rollout of renewable energy will continue and even accelerate.

Additionally, in the electricity sector, demand has been significantly reduced as a result of lockdown measures, with knock-on effects on the power mix. Electricity demand has been depressed by 20 percent or more during periods of full lockdown in several countries, as upticks for residential demand are far outweighed by reductions in commercial and industrial operations. Demand reductions have lifted the share of renewables in the electricity supply, as their output is largely unaffected by demand. For the year as a whole, output from renewable sources is expected to increase because of low operating costs and preferential access to many power systems. This would mean that low-carbon sources far outstrip coal-fired generation globally, extending the lead established in 2019 (World Energy Investment 2020).

With increased capital investments in the renewable sector and higher representation of renewables in the electric sector, the path to a low-carbon future has become more desirable but uncertain as well. World leaders are now faced with a choice: Reopen economies powered by the failing fuel sources of the past, or jump-start paths toward a clean, secure and prosperous future by investing now for the long term. The bigger question is whether the expansion of renewables is sufficient to achieve the recommended 1.5°C target temperature?

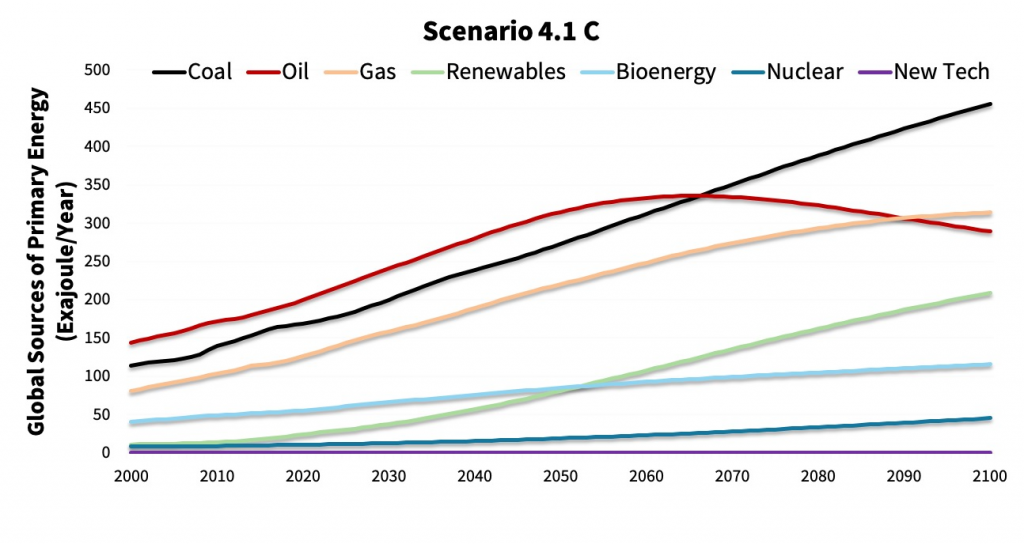

We use a scientific, credible, freely available policy simulation model to scientifically answer the question above. We observed that policy changes focused on highly subsidizing renewables, imposing a very high tax on carbon and even allowing for huge technological breakthroughs are insufficient to bend the global temperature curve from current business-as-usual to the recommended 1.5°C target temperature. These renewable energy focused changes will help us only to slow down global warming by 1.0°C (from current 4.1°C to 3.1°C) (Figure 1 and Figure 2).

Figure 1 – Business-as-Usual Scenario 4.1 C. No changes in energy supply, transport, building and industry, land and industry emissions, carbon removal. Source: EN-ROADS

Figure 2 – Scenario 3.1 C. Renewable energy highly subsidized, very high carbon tax, huge technological breakthrough. Source: EN-ROADS

To further bend the temperature curve, policy makers, investors and corporations need to do two things. First is to focus on increased energy efficiency and electrification in transport, building and other sectors. Second, is that more attention needs to be given to new technologies that help to reduce emissions or reduce the impact of emissions from existing energy infrastructure. This could include agricultural practices that sequester carbon in soils, bioenergy with carbon capture and storage, direct air capture and potentially geoengineering solutions such as stratospheric aerosol injection, marine cloud brightening, cirrus cloud thinning, or ground-based albedo modification (Figure 3).

Figure 3 – Scenario 1.8 C. A Cross-sectoral transformation is needed to hit the Paris Agreement goal. Changes in energy industry: highly subsidized renewable energy, very high carbon tax, huge technological breakthrough. Changes in transport, buildings and industry: energy efficiency highly increased as well as electrification incentivized. Changes in land and industry emissions: Highly reduced deforestation, moderately reduced methane & others. Changes in carbon removal: medium growth in technology. Source: EN-ROADS

Additionally, globally we need to increase the development and application of reporting metrices and standards that are focused on measuring emissions reductions (for all GHG emissions including carbon and methane). Organizations leading the climate reporting disclosures such as Task Force on Climate-related Financial Disclosures (TCFD) must include carbon reduction reporting in addition to carbon foot-print disclosures. Carbon reduction reporting is a key practice that Entelligent, a data platform company based in Boulder, Colorado, recommends for its large institutional clients.

Advancing energy efficiency and direct desired policy shocks such as high subsidies to renewables and a carbon tax will trigger huge shifts in corporate balance-sheets. If there is global desire to bend the temperate curve to the 1.5°C target, financial stakeholders such as banks, asset managers, institutional investors, pension funds and portfolio managers must take action and integrate knowledge and information on climate transition risk with their investment strategies.

The policy, supply chain and energy mix disruption shocks that we are experiencing related to COVID-19 are classified the same as climate change — as an unpredictable unknown. Accelerating change and bending the temperature change curve demands that we immediately account for such shocks by accounting for climate change risk.

Article by Pooja Khosla Ph.D., Vice President Client Development at Entelligent. Dr. Khosla is an economist, econometrician, and mathematician who has deep knowledge to build investing solutions. She has extensive experience in predictive modeling, microfinance and designing impact investment tools. Khosla has been working on impact solutions since 2003 both nationally and internationally. Khosla has been working with Entelligent since 2016 developing Entelligent’s data science team, Smart Climate technology, Smart Climate Indices as well as additional climate risk related products. She is one of the inventors of patented Smart Climate technology. Khosla has several publications in economics, impact investing and microfinance. Besides designing sustainability products Khosla has an active teaching career training student in economic applications and data science. Khosla holds a Ph.D in economics, and master degrees/diploma in three disciplines including economics, statistics and public relations.

References

Liu Z, Deng Z, Ciais P, Lei R, Feng S, Davis SJ, Wang Y, Yue X, Lei Y, Zhou H, Cai Z. Decreases in global CO $ _2 $ emissions due to COVID-19 pandemic. arXiv preprint arXiv:2004.13614. 2020 Apr 28.

IEA (2020), World Energy Investment 2020, IEA, Paris https://www.iea.org/reports/world-energy-investment-2020

Watts, J. We have 12 years to limit climate change catastrophe, warns UN. The Guardian. Oct 2018. https://www.theguardian.com/environment/2018/oct/08/global-warming-must-not-exceed-15c-warns-landmark-un-report

Ip G. Coronavirus Is Buying Time on Climate Change. Will We Make Use of It?. The Wall Street Journal. May 2020. https://www.wsj.com/articles/coronavirus-is-buying-time-on-climate-change-will-we-make-use-of-it-11590676308

Koop. F. ZME Science – Is the coronavirus crisis accelerating the shift to renewables? May 2020. Is the coronavirus crisis accelerating the shift to renewables? https://www.zmescience.com/science/coronavirus-crisis-accelerating-renewables-01052020/

World Resources Institute – 3 Reasons to Invest in Renewable Energy Now https://www.wri.org/blog/2020/05/coronavirus-renewable-energy-stimulus-packages

Jacobius.A. Energy assets continue plunge as industry sees a shift. Pensions&Investments .June 2020. https://www.pionline.com/largest-money-managers/energy-assets-continue-plunge-industry-sees-shift?utm_source=pi-alternative-digest&utm_medium=email&utm_campaign=20200602&utm_content=hero-headline&CSAuthResp=1591125073964%3A0%3A390917%3A391%3A24%3Asuccess%3A7B482384AB8B04C452A1F89FE9183559

Financial Stability Board 2016. Recommendations of the Task Force on Climate-related Financial Disclosures. Financial Stability Board, Basel, Switzerland (2016).

Climate Interactive En-ROADS https://www.climateinteractive.org/tools/en-roads/