• Urgent grid modernization needed: Decades-old infrastructure is under strain from AI, EVs and rising demand—risking a potential significant outage.

• Capital expenditure cycle has kicked off: Utilities boosted their capital expenditures by 12.6% in 2024 – with an 8% increase projected for this year.

• Investment opportunities span multiple industries: Our portfolios hold 6 stocks leading the way in software, generation and storage

On April 28, 2025, a massive midday blackout swept across most of Spain and Portugal, extending into parts of France. Anyone who has experienced a power outage knows how disruptive it can be, as most of our daily activities and work routines depend heavily on reliable electricity. Maintaining a consistent and reliable power supply requires carefully balancing electricity generation with demand across the regional grid. And achieving this balance requires a different set of technologies and approaches today compared to those used 50 to 70 years ago.

Much of the current power generation and transmission infrastructure was built in the 1960s and 70s and is approaching the end of its typical life. Add in the increasing demand from the use of AI, cloud computing, electric vehicles and cryptocurrencies, and the potential for the U.S. to incur significant outages like the one in Spain isn’t out of the question.

The need to update and modernize the grid has kicked off a cycle of capital investments, with our portfolios holding several companies that are key players in this effort. At Parnassus, our investment process focuses on high-quality business with durable competitive advantages, increasing relevancy, strong management teams and sustainable business practices. In this paper, we highlight a range of companies driving or benefitting from improvements to the electricity grid infrastructure and explore how the landscape for electricity generation has evolved over the last 20 years.

Electricity supply and demand evolution since 2005

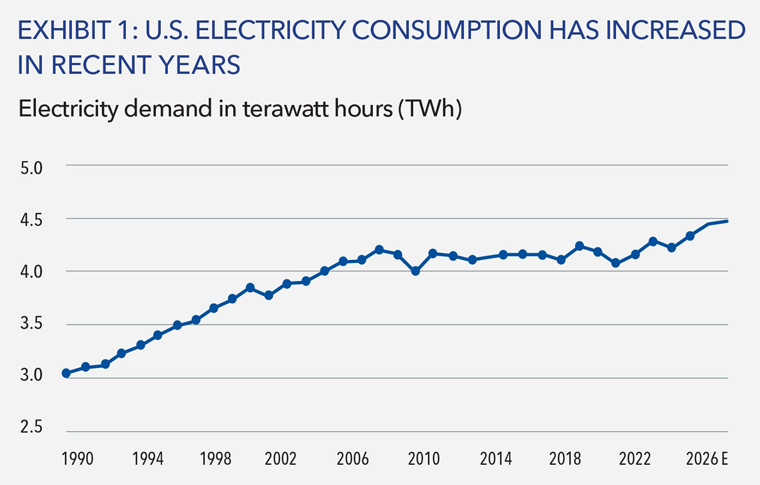

Over the past 20 years, increases in electricity demand have been largely offset by corresponding improvements in energy efficiency, many of which were driven by the “Energy Star” programs that created more efficient appliances and household items. As a result, overall U.S. electricity demand was relatively flat from about 2005–2017 as shown in Exhibit 1 below, even as the U.S. economy expanded by 141% during the same period.1 Since 2020, however, energy demand has been trending up.

Source: U.S. Energy Information Administration, May 2025. Data for 2025-2026 are estimates.

Around 2005, the U.S. also began diversifying power generation sources towards cleaner energy. Exhibit 2 (at top of the page) shows how coal, which used to be the most common source of power, has decreased from 53% of the electricity generation sources in 2000 to less than 20% in 2023. At the same time, renewables and natural gas have grown from 23% of the electricity generation sources in 2000 to more than 60% in 2023. This shift in power generation sources from coal to natural gas and renewables also brings the opportunity for increased resilience of the electrical grid because it requires the power grid to shift from a one-way distribution of electricity to a two-way flow, in which electricity flows both ways from traditional power plants to consumers and businesses using solar panels and energy storage systems.

Investment opportunities spanning several industries

Efforts are underway to modernize the grid, adding the resilience and flexibility needed to better optimize the new power generation sources. S&P Global reported in January 2025 that utilities boosted their capital expenditures by 12.6% in 2024. This increased investments in upgrading and expanding power generation, transmission and distribution networks.2

That upward trend is expected to continue, with an 8% increase projected for this year, bringing total spending to $202 billion. These investments will focus on modernizing critical infrastructure such as substations, transformers, transmission and distribution lines, and the development of energy storage for clean-energy sources.

We view these improvements as a once-in-a-generation opportunity to redesign and renovate our energy infrastructure. This overhaul will enable the grid to more effectively distribute various sources of energy precisely when they are needed. The resulting investment opportunities are interesting because they span different industries and could reshape them for decades to come.

A core element of this grid infrastructure modernization involves advanced electrical equipment and components that support a “smart grid” that can proactively manage demand response, monitor energy load, handle power outages and detect faults. Connecting smart meters to a smart grid enhances data exchange and operational control. Hubbell (HUBB) stands out as a key solution provider in this critical area. With a legacy spanning more than 137 years, Hubbell is the market leader in selling electrical components to utilities. This highly fragmented market favors companies like Hubbell with its scale and strong reputation. Its ability to provide end-to-end solutions from meters to substations helps create resilience to extreme weather events.

Additionally, special semiconductor chips are central to enabling the smart grid and are required to provide highly efficient and reliable power-management solutions. Monolithic Power Systems (MPWR) provides a range of high-performance power- management solutions, including smart meters that allow for two-way communication and backup-power solutions to enable continuous operation during power outages. They also offer components that efficiently convert renewable power sources and battery management solutions that help stabilize the grid. Their power conversion technology also supports EV chargers, enabling the growth of electric vehicles as part of the modern grid. The company has a strong track record of market share gains driven by technological leadership and being a first mover on power management for AI.

On the supply side, significant improvements in solar technology, wind turbine efficiency and energy storage have drastically reduced costs and improved the performance of renewable energy sources. The landscape has evolved as new firms have entered alongside existing players to address the growing demand from data centers and need for clean and resilient energy sources. Brookfield Renewable Corp. (BEPC) operates one of the largest pure-play global platforms for renewable energy sources. The company’s established relationships with major corporate buyers of clean power highlight its strong market position and ability to provide decarbonization solutions at scale. More than half of Brookfield’s revenue comes from hydroelectric power, an energy source that is hard for newcomers to replicate. We also like the company’s extensive portfolio beyond hydro, such as wind and solar power as well as storage facilities.

The shift toward renewable sources also requires addressing the inherent intermittency of wind and solar power. That’s why natural gas is considered a crucial bridge fuel. It produces less carbon dioxide than coal and oil and can reliably meet surges in energy demand. This has created strong demand for turbines that convert natural gas into electric energy from companies like GE Vernova (GEV). The company is a market leader; its technology base helps generate approximately 25% of the world’s electricity. They have a comprehensive suite of products, services and software solutions that address the key challenges and opportunities in modernizing the grid, including a platform that helps utilities orchestrate the distribution of energy resources, supporting grid stability and optimization through AI-powered analytics. Importantly, they also offer cybersecurity solutions specifically designed for the energy sector.

Modernizing grid infrastructure also creates opportunities for companies that provide the intelligence layer for the new energy ecosystem. Two European companies, Schneider Electric (SU-FR) of France and Siemens (SIE-DE) of Germany, are leaders in this area, offering a wide range of technologies, software and services that support flexible and resilient grid operations. We find Schneider compelling as a global leader in energy-management and automation solutions because its innovation-driven product suite creates a wide economic moat in diverse end markets such as data centers, industrial facilities and homes—all critical nodes in the evolving grid. Siemens also plays a vital role, providing both hardware and digital solutions that have significant exposure to key secular growth drivers such as industrial automation, smart infrastructure and mobility.

A Long-term investment perspective

Looking forward, AI’s integration into the economy is expected to be a significant driver of electricity demand. This anticipated surge in demand from AI, combined with our existing mix of renewable and transitional energy sources, is shaping a capital investment cycle that presents compelling opportunities. How much, how long and how extreme the cycle is will depend on how investments in AI, data centers and cloud computing continue. We are watching for any acceleration or deceleration of capital expenditures over the next 3 to 5 years, as well as any regulatory changes that impact the pace of development. Most critically, a faster pace of permitting will help accelerate the pace of projects. As investors, we must weigh the risks tied to extreme weather events, rising electricity demand and the ongoing modernization of the grid. The need for resilient infrastructure is more urgent than ever — making this a unique opportunity for investors to play a role in shaping the future of a more sustainable and resilient power grid.

Building out the grid sustainably

Sustainable business practices are important as companies build out the electric grid’s infrastructure. As important as it is to ensure that the grid can meet rising electricity demand to avoid blackouts, this work must be accomplished while addressing material sustainability considerations. Companies should effectively manage their own risks, such as labor management, operational pollution and power efficiency. For example, companies that disclose how much of their new products contribute to energy efficiency can help in monitoring energy usage, reducing the stress of rising energy consumption on the grid and contributing to net-zero emissions goals that companies have set. When evaluating companies, it is important to assess how companies are innovating with sustainable practices, such as developing more energy-efficient products. Labor practices also warrant close attention. Ensuring fair treatment of employees is essential in preventing high turnover, potential reliability issues and workplace injuries. For example, after the deaths of three GE Vernova contractors in 2023, the company has taken steps to strengthen its safety strategy. This included a shift from a set of safety principles to more specific rules to ensure the safety of its employees, contractors and partners. The enhanced strategy also places greater emphasis on reporting and investigating near misses and injuries to prevent future incidents.

Article by Lori Keith, Director of Research, Portfolio Manager at Parnassus investments; Andrew Choi, Portfolio Manager, Senior Analyst at Parnassus investments; Michael Beck, CFA, Senior Analyst at Parnassus investments. Originally Published by Parnassus in June 2025.

Footnotes:

[1] US Energy Information Agency “Monthly Energy Review” January 2025. Federal Reserve Bank of St. Louis.