We’re losing ground in the climate fight at the worst possible moment. As the current federal administration continues to deny existential threats, defund adaptation efforts, and deregulate safeguards, decades of progress in protecting our environment are being eroded right in front of our eyes. In the face of this wide-scale regression, it’s understandable to fall into despair. As we look for ways to move through this moment, we find that hope for a brighter future is abundant at the local level. In the wake of these challenges, manylocal communities are doubling down to protect their neighbors from climate disasters, strengthen mutual aid, and create a fair and equitable economic system. Within that economic support, one of our greatest tools for strengthening local economic health, combating the climate crisis, protecting frontline communities, and building a sense of belonging lies in the humble credit union.

A better way forward

Credit unions are led with an open-hearted pathos: people helping people. They are mutualist organizations predicated on the notion that we can have a banking system that prioritizes community well-being, not just the cold accumulation of exponential growth for select shareholders. They prove that we can have financial success without investing in funds that threaten the air and water we depend on, and that we can grow with, not despite each other. Reinforcing this commitment, the current NCUA Chairman, the federally appointed monitor and regulator of all US credit unions,has confirmed that credit unions must prioritize supporting low-income areas and tackle local climate risks.

The revolutionary idea that credit unions introduced to the American economy was that a financial institution could be owned by the community members themselves and could operate on a not-for-profit model. Not-for-profits take any profits generated and immediately reinvest them back into their membership, leading to a direct symbiosis within the member base. There are many similarities between a credit union and a traditional bank; however, this is a major differentiator that distinguishes the two.

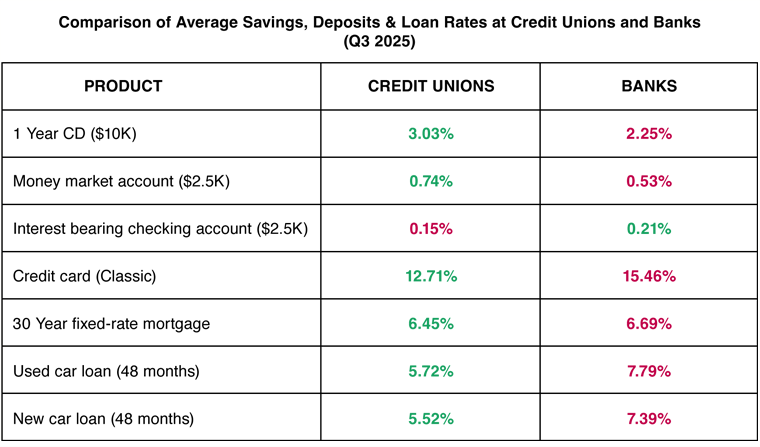

As a result of their not-for-profit operating model, credit unions consistently offer better interest rates to their members compared to traditional banks, on everything from interest earned on a savings account to lower interest on mortgages and vehicle loans.

Data extracted by NCUA from S&P Global Market Intelligence databases (https://www.spglobal.com/marketintelligence) on October 7, 2025. The data represent interest rates reported by active banks and credit unions for the last Friday of the quarter (September 26, 2025).

In addition to their increased financial benefits that strengthen local economies, the direct interviews below highlight how credit unions are uniquely positioned to support the environmental and social needs of the communities they serve. Recognizing how financial inequities exaggerate the threats of the climate crisis, MariSol Federal Credit Union in Phoenix, AZ, developed a unique and deceptively simple solution to help their majority low-income member base survive in an increasingly hostile climate. “The Phoenix Metro saw 113 consecutive days over 100 degrees in 2024,” said CEO Robin Romano, when interviewed this spring. These temperatures are more than just uncomfortable; they are an active threat to life. In 2024 alone, over 600 residents of Maricopa County died from overexposure to high heat. “Keeping cool costs money, and low-income houses cannot afford to pay rent and escape the heat,” Romano continued. To prevent future loss of life or brownouts of the electric grid, MariSol FCU launched their solar and energy efficiency lending products in late 2022, radically offering all members the same low interest rate, regardless of their credit score.

“Doing this work is mission-driven; it’s a simple economic decision based on fairness,” said Romano. Since the team at MariSol launched this program, the vast majority of their energy efficiency loans have gone directly to low-income households. “We’re not doing anything outside of what a credit union should do,” Romano said proudly. “We exist to meet the needs of our communities and listen to our members, and that’s exactly what we’re doing.”

Clean Energy Credit Union attributes their success to operating with a simple vision: they want to fund the future and do so ethically. Through their work of solely funding affordable clean energy projects, over 13,000 to date, values-aligned members from 49 states have found a new financial home. “For my team, ethical banking was simply the default path that we took as a mission-aligned credit union. You can’t have a great environment unless you take care of the people in it,” said CEO Terri Mickelsen in an interview for this article. The team at Clean Energy pursues this mission through their Clean Energy for All Program, which prioritizes the unique energy needs of BIPOC and low-to-moderate-income households.

“We have done $3 million in loans through the Clean Energy for All Program, primarily for smaller projects like home insulation and building envelope work, which can have a big impact on these families,” Mickelsen continued. The Clean Energy CU staff takes care when reviewing applications with low credit scores, tailoring rates to the individual needs of each member by examining details like income verification, debt-to-income ratio, length of residence and employment, and even projected utility bill savings before creating a repayment structure that the member can actually afford. Unique programs such as these are natural for credit unions because of their collectivist mission to uplift communities, and they prove to be successful business choices. While the current delinquency rate on consumer loans from commercial bank customers hovers around 2.76%, to date, Clean Energy CU has had a less than 1% delinquency rate on their lending products, easily dispelling the false assumption that those with less money are untrustworthy.

Credit unions not only add financial and environmental resilience to communities, they have the power to heal. On the farthest islands of Hawaiʻi, the team at Kaua‘i Federal Credit Union is working to rebuild generational wealth for their native community, and helping Native Hawaiians build homes on Native Hawaiian Land. This is no easy task, as a single-family home on Kaua’i sells for amedian price of $1.4 million, while the median annual income pales in comparison at $41K. As a result of these inequities, for the first time, a majority of native Hawaiians nowhave to live outside of Hawaiʻi.

“Housing is one of the most pressing challenges facing local families today. For us, affordability isn’t just a low-income issue — many middle-class families, teachers, and working professionals are also being priced out, and when people who serve our community can’t afford to live here, it affects the entire fabric of our island,” said Nikki Ige, Kaua’i FCU Chief Lending & Impact Officer, in an email interview this fall. Seeking to prevent further outward migration and restore community capacity, Kaua’i FCU worked with Filene Research Institute, Hawaiian Community Assets, and the Federal Home Loan Bank of Des Moines to develop an assistance program that provides local families with a grant for a down payment and closing costs for a new home.

“We’re proud of the programs we offer to help our members stay rooted here, but there is still much more to be done,” said Ige. “Creating opportunities and providing resources to our community, especially for those historically excluded or disadvantaged, is an original credit union ideal, and seeing our entire island thrive is what continues to be our driving force.”

How to move forward with action

These three cases show how climate action and mutualist progress can flourish even in the face of broad government regression. “Community-centric businesses like co-ops and credit unions operate like an underground web of reciprocity for the common good,” said Wall Street alumna Elsie Maio, whose insights were the key impetus for this research. An advisor to values-centered leaders for decades, Maio calls credit unions a “best kept secret” that could help stabilize the precarious financial well-being of middle and working-class Americans, especially in today’s K-shaped economy. “Too long the financial services industry has piped the ‘cheap money’ that flows from Americans’ low-interest checking and savings accounts into big banks’ global casino. Instead, with public awareness and easier access, credit unions could become Americans’ way to reclaim their deposits for the well-being of their own back yards.”

Honoring the power that we possess when we work as collaboratives, as real communities, is key not only to maintaining our well-being and safety; it’s our best tool to fend off despair. Don’t believe them when they say we have to go back. We steer our own ships, we help our neighbors and we’re not backing down.

Article by Garrett Chappell, founder of Pasqueflower Consulting, LLC, is an advisor on sustainability programming in the credit union industry, and nonprofit organizational development. He presented the business case for sustainability programming at the United in Sustainability Conference at the United Nations in 2025. Contact him at- garrett@pasqueflowerconsulting.com