The world is short on power ― and time.Global electricity demand jumped 4.3 % in 2024, nearly double the past-decade average, and is projected to increase at 4% annually through 2027. From AI clusters in Virginia to air-conditioner peaks in India, grids are groaning worldwide. Governments now face a dual imperative: keep bills affordable today and accelerate the deployment of electricity solutions to unlock unprecedented economic development opportunities.

The challenge of meeting load growth occurs against the backdrop of significant global restructuring and change ― and a retrenchment in local supply chains. The Carlyle Group frames this race for secure, home-grown energy as the emerging “New Joule Order,” arguing that nations will pivot toward local, clean electrons to cut import risk and price volatility.

How to meet load growth quickly and competitively

In most regions, renewables paired with batteries have recently become the fastest and least disruptive solution to meet rising electricity demand while maintaining affordability. Utility-scale solar can be financed and built quickly, with grid-scale batteries completed in just 100 days — while new gas plants often take five years amid soaring turbine prices and limited EPC bandwidth.

Grid-enhancing technologies (GETs) unlock hidden capacity on existing wires — facilitating new construction and better asset utilization of existing generation on constrained grids. The U.S. Department of Energy’s Innovative Grid Deployment Liftoff Report shows that commercially available GETs — such as advanced conductors, dynamic line rating (DLR), power flow controllers, and distribution automation — can unlock 20-100 GW of peak transmission capacity using existing infrastructure. These upgrades deploy quickly at a fraction of new transmission costs. Similar initiatives are underway globally: India’s Green Energy Corridors and Brazil’s ISA CTEEP are deploying GETs to alleviate congestion and accelerate more clean energy integration.

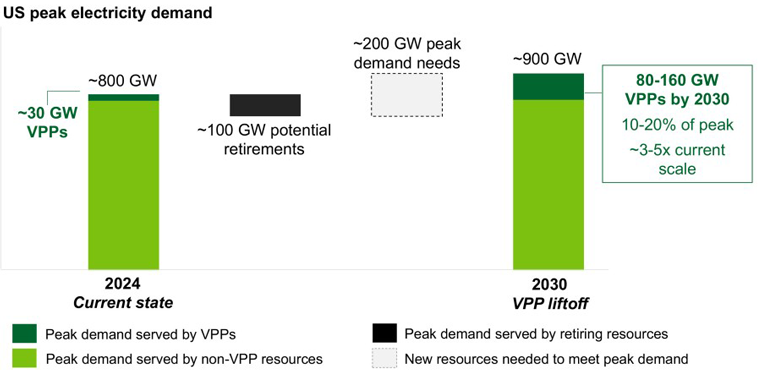

Source: U.S. DOE Pathways to Commercial Liftoff: Virtual Power Plants 2025 Update

At the same time, demand flexibility offers an invisible but key pillar of affordable, resilient clean energy systems. Virtual Power Plants (VPPs) aggregate flexible industrial demand, smart thermostats, electric vehicle chargers, and behind-the-meter batteries into coordinated fleets that act like a dispatchable power plant. According to the DOE VPP Liftoff Report, we can have 20% of peak loads in the U.S. be dispatchable by 2030, avoiding up to $10 billion per year in transmission and distribution infrastructure costs. Because VPPs are software-enabled, they can scale in months, not years, and their capital is largely private — households and businesses buying devices with advanced features they already want.

Firming resources are critical compliments to renewables build outs—for high-capacity factor electricity consumers such as data centers. Natural gas will be a part of this mix over the decades to come and addressing methane emissions must be a global priority. Furthermore, clean firm power sources such as advanced nuclear, enhanced geothermal systems (EGS), long-duration energy storage (LDES), and pumped hydro can play an increasingly important role in balancing grids as variable renewables increase their share. However, these technologies face a bankability gap: capital intensive, unfamiliar to financiers, and lacking dependable revenue within current rules. With the right policy support and financial innovation, these clean firm resources can move from promise to deployment, anchoring the reliability of grids over the next decade.

Five policy lessons in the age of load growth

Against this backdrop, the real deployment chokepoint is no longer technology availability but policy execution. Interconnection queues, permitting timelines, offtake structures, and public-finance tools all hinge on government action. In scaling the U.S. Department of Energy’s (DOE) Loan Programs Office (LPO), we’ve seen firsthand how smart policy can crowd in private capital and accelerate deployment. Tailoring these efforts to meet surging load growth while prioritizing affordability can transform risk into a competitive advantage:

1. Put Affordability First.

Low, predictable costs must be the north star of any national strategy. Families around the world are feeling the squeeze: the average U.S. electricity price climbed to a new high of 12.99 ¢/kWh in 2024 (16.48 ¢/kWh for households) — up 22 % in just five years, while a “typical” UK household will still pay about £1,568 a year for power in 2024 (28.6 ¢/kWh). The fastest tools — utility-scale renewables paired with storage, grid-enhancing technologies (GETs) and virtual power plants (VPPs) — are also the cheapest. Governments should remove barriers to fast deployment of these low-cost tools while phasing out subsidies and improving public messaging — reserving separate budgets and timelines for commercializing next-gen technologies.

2.Define the Goal, Not the Tech.

In almost every case, government should set technology-neutral targets and let markets decide how to hit them. In the United States, the new §45Y/§48E “tech-neutral” clean-electricity tax credits were originally designed to reward any zero-emission project instead of listing preferred technologies one by one. Across the Atlantic, the UK’s Contracts-for-Difference (CfD) auctions follow the same principle: all eligible resources compete on price.

This neutrality matters. When policymakers stay agnostic, developers chase clear price signals, innovation flourishes, and consumers pocket the savings. At LPO we lived by the mantra “private-sector led, government-enabled.” Our role was to set the goalposts and clear away red tape; entrepreneurs and industry responded with over $400 billion in applications spanning grid-scale batteries to small modular reactors.

3. Proactively Engage Innovators.

Money alone doesn’t lure entrepreneurs; clarity, speed, and relationship building do. When LPO cut a 100-page application into a two-step form, published plain-language guides, and started calling 100s of CEOs directly, its deal flow jumped from one application a quarter to two every week. Crucially, that rapid expansion didn’t raise risk: the portfolio’s lifetime default rate remains ~3% and is predicted to go down to 1.5% over the next decade.

The lesson travels: helping founders navigate permits and paperwork, and deepening investor understanding can turn public money into a magnet for private capital. Whether the target is transmission upgrades, VPP aggregators, or critical minerals refining, governments invest in relationships with the most courageous entrepreneurs and innovators can crowd in billions from first-time applicants instead of just recycling subsidies through incumbents.

Source: Investing with LPO Toolkit, 2024

4. Rebalance Risk & Return.

Geothermal reservoirs, sustainable aviation fuel (SAF) production, and critical minerals refineries won’t scale on low-cost senior debt alone — but they can clear investor hurdles when cheap public capital aligns with evaluating the risk of projects using a private sector lens. At the Loan Programs Office (LPO) at the DOE, we built an Investing with LPO Toolkit to explain how our commercial and technical diligence process was rigorous enough to derisk energy investments, serving as a “golden ticket” for companies and “stamp of approval” for investors.

Other public finance institutions are following a similar path. Australia’s Clean Energy Finance Corporation reports every public dollar it lends crowds in $2.50 of private co-investment, often via subordinated debt that boosts equity IRRs without raising taxpayer exposure. Canada’s new Growth Fund goes one step further, offering first-loss carbon contracts for difference that guarantee a carbon-price floor.

In 2021, LPO had $40B in unused authority that had barely been touched in a decade. By January 2025, we had committed $108B for clean energy and manufacturing projects across America. We left with another $324B of active applications across almost 200 high quality applicants. Our rigorous outreach combined with relatively low-cost private sector engagement efforts (like the Liftoff reports, Deploy summits) catalyzed industry and investor action. And we were cost neutral for American taxpayers. An affordability-focused energy strategy doesn’t have to break the public bank.

Putting it into practice, constructively

A new non-profit — Constructive — aims to help governments put these lessons into practice. Drawing from our experience from DOE and industry, the Constructive team designs data-rich engagement platforms that build alignment and crowd in private capital towards clean energy priorities. Our shared goal is to deliver reliable, affordable energy while slashing emissions and strengthening local supply chains. The tools exist. The playbook is proven. What matters now is execution — and for that, there is no time to lose.

Article byJigar Shah and Johan Wagner. The authors would like to thank Louise White for her contributions to this article.

Jigar Shah is on the Board of Constructive and is a Senior Fellow at the World Resources Institute. Mr. Shah was the director of the Loan Programs Office in the US Department of Energy from March 2021 to January 2025. He is the author of the book “Creating Climate Wealth: Unlocking the Impact Economy.”

Jonah Wagner is the President and Co-Founder of Constructive. He is the former Chief Strategist at the U.S. Department of Energy’s Loan Programs Office, where he led portfolio strategy and co-led the DOE Pathways to Commercial Liftoff and Deploy efforts. He also held the position of Principal Assistant Director for Clean Energy at the White House Office of Science and Technology Policy, overseeing cross-agency energy innovation policy priorities. Previously, Jonah was an Associate Partner at McKinsey & Company, where he specialized in public finance, infrastructure, and customer experience design. He also served in nonprofit, government, and early stage business leadership roles advancing public infrastructure innovation across Latin America, New Zealand, and India. He holds an MBA from Harvard Business School and an A.B. from Princeton University’s School of Public and International Affairs.